1.The market continued to fluctuate last week, and the exchange’s deposit and withdrawal volume was relatively active. The exchange has a net withdrawal of 22,800 Bitcoin this week, with a reserve balance of approximately 2,456,700. The BTC reserve balance on the exchange is currently at a three-year low.

2.The bargaining chip in the market continues to drop sharply. From the perspective of illiquid supply and exchange withdrawals, the market is facing a more severe crisis in the supply of chips. This kind of supply crisis will in the future prompt prices to rebalance supply and demand, through rising prices.

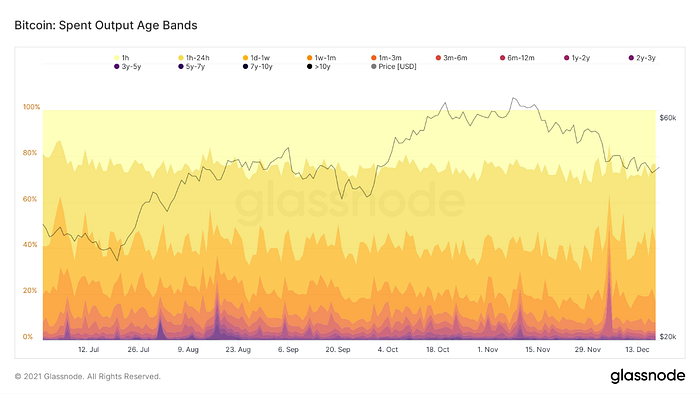

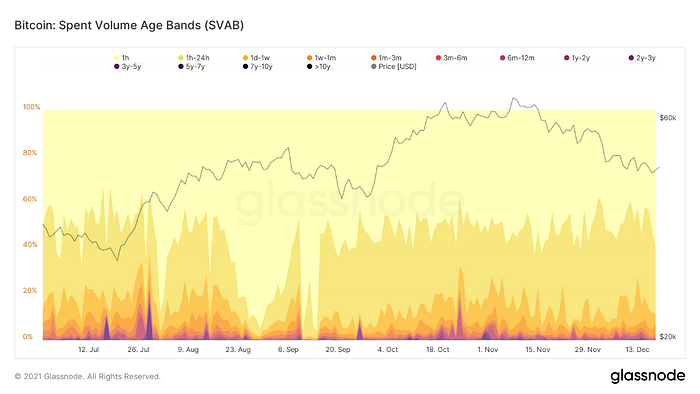

3.LTH supply, CDD, SOAB, SVAB and other indicators all reflect that long-term holders at this price level have not sold their Bitcoin significantly. We can assume that they are still not satisfied with the current price, and covering the sale will lead to a decrease in the selling pressure in the market — which is conducive to the subsequent upward market.

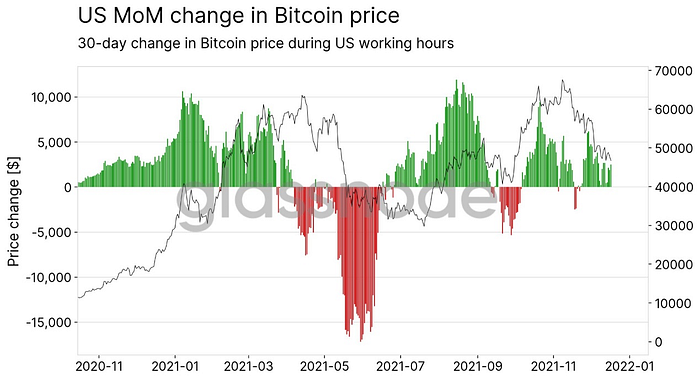

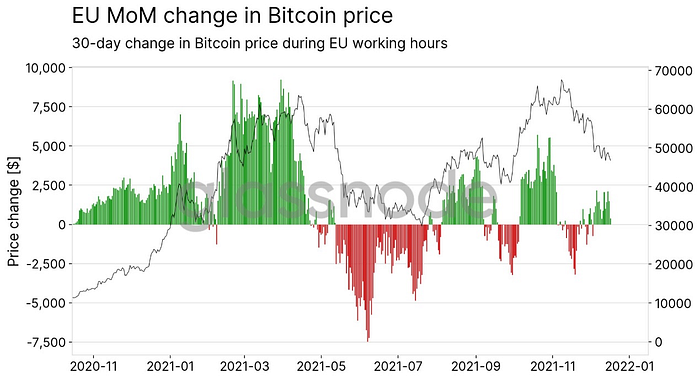

4.By dividing investors in different trading time zones, Bitcoin trading volume has been relatively high during the Americas and Europe trading time since November, while trading volume during the Asian trading time has been very poor. This suggests that the group of investors currently selling Bitcoin are mainly Asian investors. Considering the large number of institutions(exchange) in mainland China facing liquidation at the end of December, this may be related to the current frenzy of Asian investors looking to “cut their losses”. This also indicates that after the peak of this wave of “cutting”, the short-term selling pressure will drop significantly and the selling cycle is nearing its end.

5.The current market sentiment that of extreme fear, and history suggests that the market will perform better in the coming months. Bitcoin prices and RSI also showed bottom divergence signals.

6.Given that the fundamentals remain healthy, this report considers this pullback to be a healthy market adjustment, which does not change the long-term trend of Bitcoin. This pullback also provides a rare opportunity for layout, as the current sell-off is gradually weakening, and we continue to be bullish on the future market. At the same time, this report believes that the current indicators are still on the low side of normal and have not yet reached their most frenzied stage. Therefore, the time cycle of the current bull market is extending, and the market is expected to return to the upward track in the first half of 2022.

I. BTC Fundamental Analysis:

Last week, the exchange BTC reserve balance continued to maintain a net outflow trend, with a net outflow of about 22,800 Bitcoins in a single week and the remaining BTC in centralized exchange is about 2,456,700. (Note: the data statistics caliber is Glassnode, the data is dynamic data, and the historical data will be updated with the algorithm iteration). The current centralized exchange BTC reserve balance is still at its lowest level in 3 years. This general trend has not stopped since the “312” event (March 12) in the industry in 2020.

Chart 1: The BTC reserve balance of centralized exchanges showed a downward trend last week, with a net withdrawal of more than 22,800 Bitcoins in a single week

Chart 2: The broad cycle trend of BTC reserve balance outflow from centralized exchanges has not changed

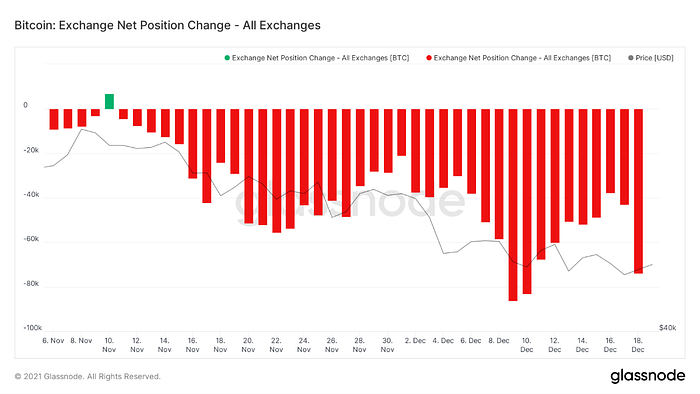

Looking at the last 30 days of net exchange position movements, the 30-day cumulative net position became continued to expand in the negative range with a value of -73,762 Bitcoins. Exchange net position movements have been in net outflows since mid-to-late July (red bar chart below). This trend reflects the major cyclical trend of tradable chips in the market and is a core cornerstone of bullish bitcoin fundamentals.

Chart 3: Changes in the exchange’s net position continue to expand in the negative range, reflecting the general trend of relatively strong buying demand

Looking at this from another angle, it is also clear that the market is facing a chip supply crisis.

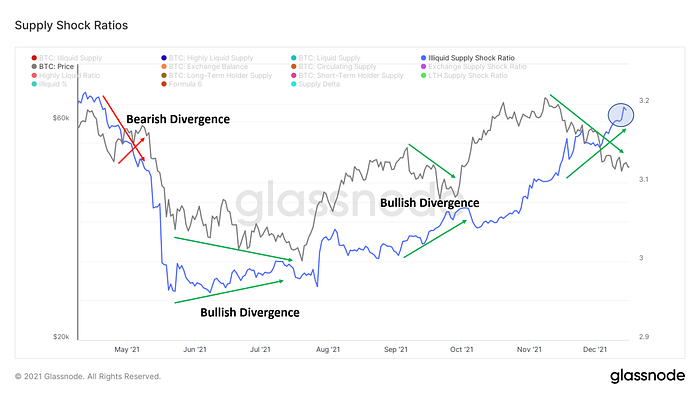

Illiquid supply refers to the amount of bitcoin in an illiquid state. It is a measure of the number of Bitcoin that have never flowed out or have flowed out in small amounts after flowing into certain addresses. These characteristics can reflect the willingness of investors in the market to hold Bitcoins.

This indicates that the market pullback, smart funds are constantly collecting chips, the supply of chips on the market has dropped sharply compared to before and after “519” (May 19). The illiquid supply shock ratio indicator is higher, indicating that the numerator is increasing and the denominator is decreasing, making the supply crisis more obvious. The current illiquid supply shock ratio indicator is showing a bullish divergence. Usually, this is a sign that long-term investors in the market are taking advantage of the downtrend to absorb chips at lower levels.

Chart 4: There is a bullish bottom divergence between the illiqduid supply shock ratio and the Bitcoin price, and the fundamental bullish trend remains unchanged.

Long-term holders have maintained a fairly high level of rationality during this pullback. We can observe this phenomenon from indicators such as LTH supply, CDD, SOAB, and SVAB, as follows.

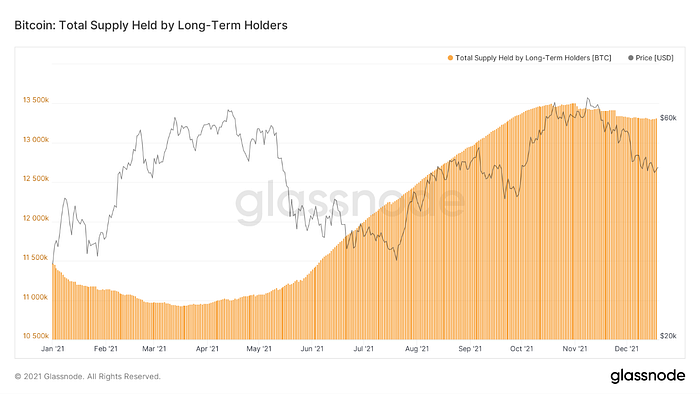

Long Term Holder Supply (LTH Supply) reflects the sum of positions held by holders with UTXO greater than 155 days in bitcoins outside of exchanges. The current round of Long Term Holder increased holdings started in late April and temporarily ended in late November, with a cumulative increase of about 2.6 million and a maximum position of 13.5 million Bitcoins. As of press time, LTH still holds about 1335 Bitcoins, relative to the peak only down about 150,000 Bitcoins. The peak selling strength (7-day ringgit) is only 0.6%, much lower than the peak of multiple selling in the past three years. A substantial chip sale has still not been carried out. A large number of chips are still held by long-term holders. This indicates that long-term holders are still not satisfied with the current price and are not willing to sell a large number of chips at this position during this round of decline. In turn, it indicates that the current substantial market selling pressure mainly comes from short-term holders.

Chart 5: The positions of long-term holders does not sell significantly in this callback, and there are signs of slight increase in holdings in the near future.

Chart 6: The biggest recent selling strength of long-term holders (7-day month-on-month) is only 0.6%, and the willingness to sell is very low.

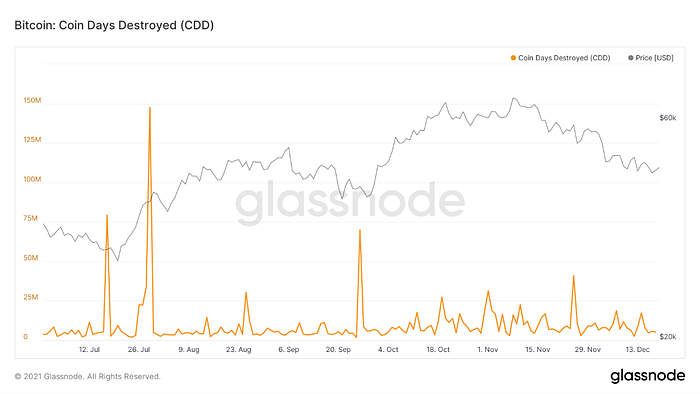

CDD can reflect the willingness of holders to sell Bitcoin. This indicator is the product of the holding number and the holding data when the UTXO of the holder is burned. The greater the holding number, the longer the holding time, and the higher the CDD value at the time of destruction. When the value of this indicator is at a high level, it can reflect two possibilities. Long-term holders for a long time or “whales” with a large amount of Bitcoin are in a sell-off state. Therefore, we can judge the cyclical tops and bottoms of the market by observing the high and low positions of the CDD indicator value.

When the CDD indicator is at a high level, it indicates that long-term holders — or giant whales — are in a sharp sell-off stage, and the market is about to peak. Conversely, when the indicator is at a low level, it means that the role of selling at this time is mainly short-term Bitcoin holders or small retail investors. At present, the indicator is still very low, and the market sell-off has not yet arrived. The overall tone is that the market is reluctant to sell.

Chart 7: CDD is still in its position, long-term holders are calm, and the side shows that short-term holders are selling BTC

Spent Out Age Bands refer to the total number of times that Bitcoin holders spend (sell) their Bitcoins, divided according to the different periods of the holding time of these Bitcoins (the time from UTXO creation to destruction), and counting the time segments of these. We usually regard UTXO holdings for more than 6 months as long-term investors, with a long time span. By observing the proportion of the number of times these long-term holders sell BTC, we find that the proportion of more than 6 months has been within 5% for a long time. Recently, it is in the range of 2%-3%, indicating that the market is in the total number of transactions of selling chips. Long-term holders accounted for only a small part, which proves that their willingness to sell chips is quite low.

Chart 8: In SOAB, the proportion of more than 6 months has been maintained at 2%-3% for a long time, indicating that long-term holders are reluctant to sell at the current price.

Spent Volume Age Bands are similar to SOAB, but the difference is that Spent Volume Age Bands reflect the fraction of total bitcoin sold by investors that is older than 6 months, while SOAB reflects the fraction of sell-offs.

The percentage of SVAB that is older than 6 months is also very low, staying between 2%-3% over time. Again, this reflects the conclusion that long-term holders are less willing to sell.

Chart 9: The proportion of SVAB longer than 6 months is only 2%-3% for a long time, indicating that long-term holders are willing to hold Bitcoins.

Now that we know that long-term holders have low willingness to sell Bitcoin, but short-term holders are selling, it is important to consider which investor regions are selling more aggressively?

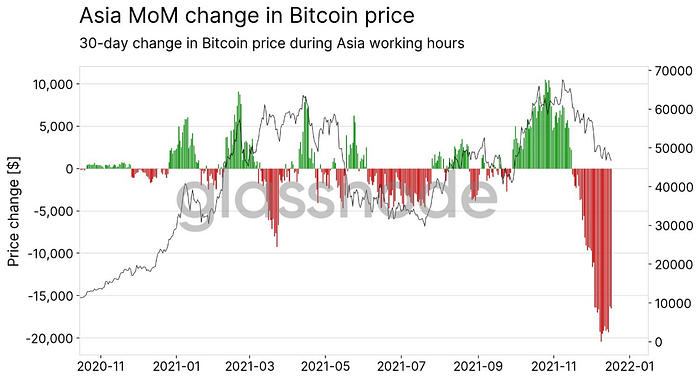

By dividing investors across different trading hours around the world into three major regions — namely American trading hours, European trading hours and Asian trading hours — most of the time in each trading session corresponds to the daytime. By counting the rise and fall of bitcoin during the three trading sessions, it can be found that the trading volume of Bitcoin in Asian trading hours since November is very poor, which is very different from the trading hours in the Americas and Europe. In the time since November, the cumulative rise and fall of the past 30 days have been combined. Most of the Bitcoin rise and fall values in the Americas and Europe are positive — that is, bitcoin rises more and falls less. Asia is not only negative, but the negative number is larger, indicating a deeper decline.

This data vividly portrays the performance of investors in different trading time zones, and Asian investors are the main force in sell-off. Since mainland China is facing very severe cryptocurrency regulatory policies this year, many cryptocurrency-related institutions face liquidation of users on December 31, many investors need to shift their investment positions, and institutions need to clarify the relationship between credit and debt, so the Asian session sells with greater intensity.

Since the Asian sell-off has a greater relationship with the retreat at the end of December, after the end of 2021, the largest peak of the Asian sell-off will pass. While the market is still fundamentally healthy, the sell-off will drop and the market is expected to usher in a sharp rise.

Chart 10: Since November, Bitcoin’s ups and downs in the Americas have been generally positive.

Chart 11: Since November, Bitcoin’s ups and downs in the Europe have been generally positive.

Chart 12: Since November, the value of Bitcoin during the Asian session has gradually declined, and the decline has been more serious since December. Asian investors have constituted the main force of sell-off.

Ⅱ. Afternoon Outlook

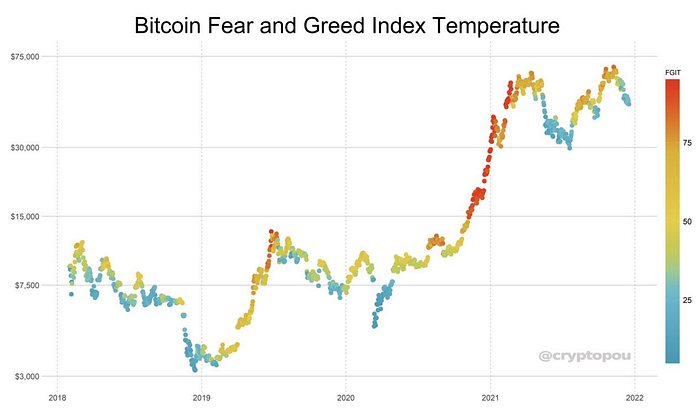

From the observation of market sentiment, the current market sentiment (Fear and Greed Index) is in the extreme fear zone. From the figure below, we can find that every time when the Fear and Greed Index is in the blue zone, it is basically the bottom zone of a round. The next six months will usher in a sharp rise.

Chart 13: The current market sentiment is in extreme fear, and the bottom is being confirmed.

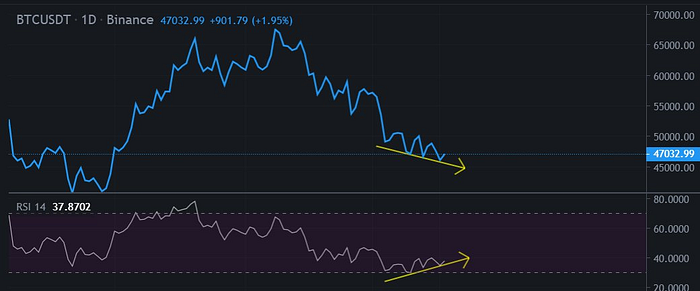

From the perspective of technical analysis, the current Bitcoin price and the RSI indicator are showing signs of divergence. The bottom divergence indicates that the buying power of the market buyers relative to the sellers has begun to increase and will start in the near future.

Chart 14: The Bitcoin price and RSI have shown a bottom divergence signal, and the price increase may kick off in the near future.

Given that the fundamentals remain healthy, this report considers this pullback to be a healthy market adjustment, which does not change the long-term trend of Bitcoin. This pullback also provides a rare opportunity for layout, as the current sell-off is gradually weakening, and we continue to be bullish on the future market. At the same time, this report believes that the current indicators are still on the low side of normal and have not yet reached their most frenzied stage. Therefore, the time cycle of the current bull market is extending, and the market is expected to return to the upward track in the first half of 2022.